Accepting credit cards should be considered by all mental health providers for ease of revenue collection they provide, but it should not be taken on without being fully thought through. While the potential benefits are high, there are costs that need to be understood. Weighing the relative value for you, your patients/clients, and your practice will be necessary to come to the right decision.

The Good

Many patients/clients actually prefer this as it simplifies their busy lives – paying their bill is just one less thing to think about.

- Many people don’t carry a checkbook anymore.

- Patients/clients can put their whole session time to good use without sacrificing time at the end to take care of payment.

- Patients/clients can easily track their expenses.

- Patients/clients can get rewards/frequent flier miles just for seeing you!

- Once you take credit cards, you can accept HSA/FSA/HRA debit cards, saving a lot of hassle for patients/clients who have these accounts.

And in addition to improving patients/client satisfaction, the benefits for streamlining your practice are mutlifold as well.

- Allows more time in session to focus on clinical matters and also allows the session to end more naturally, without spending any time on collecting payment or dealing with a forgotten checkbook or a patient’s request for a change in your policies at the last second.

- Eliminates the onerous burden of bill collection – including the cost, time and hassle of stamps, paper, toner, preparing and mailing invoices.

- Accepting credit cards allows you to be remunerated at the time services are rendered.

- Collecting payment for no-shows is easier. (Ironically there can be a reduced no-show rate as well as there is more accountability on the patient/client’s part to show up knowing that their credit card is on file.)

- Time savings: recording and depositing checks can take away precious minutes during the day.

- You’ll avoid problems with patients/clients paying invoices slowly.

- Bounced checks and dealing with collections can be completely eliminated.

The Bad

First, there is the cost in terms of the image of your practice. Some providers feel that accepting credit cards makes their practice look like too much of a commercial business, and they don’t wish to convey that.

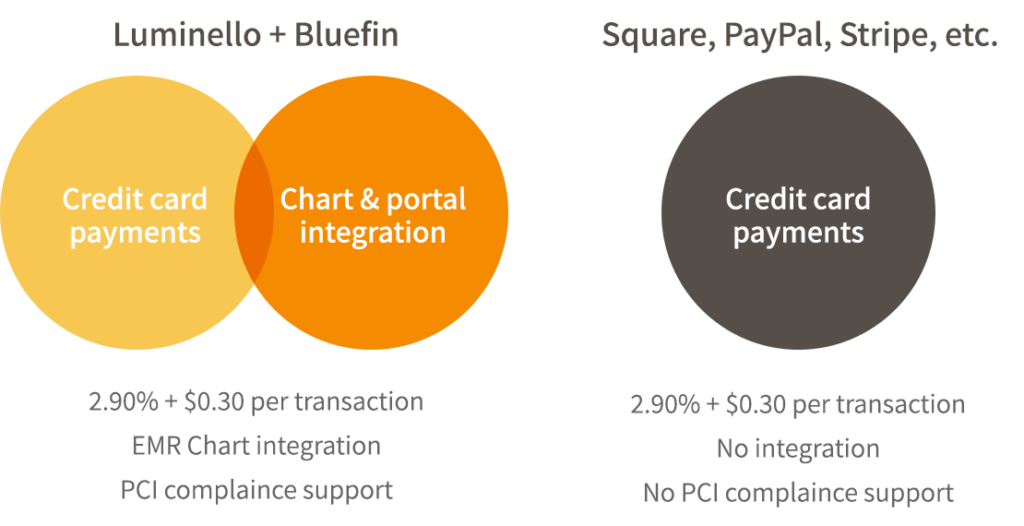

Second, there is the raw cost of accepting credit cards, and understanding the system can be confusing.

There are two systems of rates. Most merchants start off with a tiered system based on what type of card is used, but in general, you will always pay a percentage of the transaction, plus a small transaction fee. The usual rate structure is:

- Debit cards are the least expensive, but often have low limits on how much can be charged

- Regular credit cards – mid-range

- Rewards cards, such as frequent flier cards, are the most expensive. Ever wondered who foots the bill for those miles? Now you don’t have to guess – it’s not the airlines, it’s the merchant (you).

And swiping cards is typically cheaper and more efficient than typing the credit card info in; but some systems allow you to store the keyed-in entry, which can then be used on a recurring basis.

The higher the volume of credit card processing you do, the more you can negotiate your rates.

The New York Times did a nice job outlining all the players involved in the credit card processing business in their small business section.

The Ugly

Security. Security. Security.

When you accept credit cards, you have to ensure that you’re fully PCI compliant (Payment Card Industry) . Depending on how you are processing transactions, you have varying level of requirements. For example, if you swipe, do you use a terminal hooked to a telephone line, or through the internet? If you don’t swipe, do clients enter credit card numbers in a patient portal that stores that data remotely, or do you enter the numbers and store them locally? Though potentially more attractive from a business point of view, if the answer in these cases is the latter, your security requirements will be significantly higher.

For a good first step, review the requirements for small business merchants. You will likely have to self-certify that you meet the requirements that your set-up demands. If there is a breach and you are found to have been negligent, fines can range from $5,000 to $100,000 per month, whether you are a large company or a one-man show.