Enlightened Practice Podcast

In this episode, Dr. Ken Braslow and Dr. Kari Kagan talk about all things finance in running a practice. Getting the mechanics on the business side of your practice down is critical so you can take good care of your patients.

Transcript of the podcast

Ken: Hi Kari. Welcome back.

Kari: Hi Ken, thanks for having me.

Ken: Sure. It’s great to have you here today. We’re going to talk about money and all things finance related to running a practice.

Kari: Okay.

Ken: The goal being to have a viable going concern so that you can provide good quality clinical care to your clients and patients, and in order to do that, you have to know how to run a business. And we’ve talked in other podcasts about different angles on that but today we’re going to talk about how this actually works with the money coming in and going out. And to get very specific with the mechanics of it, when I was in training I was on a salary basis, and I think at the very beginning in orientation, you just gave them your checking account number and the money just showed up magically at the end of the month, or at the first of the month.

Kari: Yeah.

Ken: And that was the extent of how much I thought about it. So, it’s a little bit different when you’re running a private practice, and it’s very workable but it just requires a little bit of setup. So, we should be thinking about how do you actually take the money in, and how do you go about doing that in a way that works for your practice and works for your patients and clients, and represents how you want to run a practice that is both taking care of people and is also a business, and how do you reconcile those two. And then what should you do with the money when it comes in, and then how do you keep track of all of it. So, that’s what we’re going to talk about today.

Kari: Great topic.

Ken: And we’re going to have a special topic at the end on dealing with not money, (i.e. when people don’t pay) and how to handle that.

Kari: Yeah.

Ken: So, let’s dive in. There’s three main ways that come to mind from me to get paid. One would be cash, the other is people writing checks, and the third would be the credit card. I think in the old days, checks were how it was done typically. Of course, with checks, what’s on the check is what goes in the account. There are no fees deducted like there are for credit cards. On the flip side, with checks, you have to actually deposit them, which used to be more painful. You’d actually have to go to the bank, and stand there in the line, or go to the teller, so you were paying with your time just in terms of depositing checks.

Kari: Right.

Ken: I guess another consideration is then it was up to the patient or client to write you a check. And sometimes they do that right on time, and sometimes they don’t. So, that can be challenging. Of course, you can bring that in to the therapy and say this is good material for us to process, but there’s lots of good material to process in therapy as well and that may not be what you want to be talking about or what they want to be talking about, but it has to be dealt with.

Kari: Yeah.

Ken: So, then there’s credit cards, which I feel like nowadays everything is paid for by your credit card, or almost everything.

Kari: Right.

Ken: It’s really common place outside of therapy, just in general in life, and in the healthcare and medical related fields, so much is paid by credit cards. I think maybe 10 years ago it seemed maybe a little weird paying for your therapy or your med check with a credit card, but I sense it’s not as big of a deal now. It just doesn’t have that weird factor, but it does cost the clinician money. They don’t collect everything that they’re billing.

Kari: Right.

Ken: On the flip side, they are not spending the time collecting.

Kari: Yeah.

Ken: So, in your practice, do you find that your clients have a particular preference to pay by credit card, or check, or cash? How does that work for you?

Kari: Yeah, I find that most want to pay by credit card. It’s the most convenient, especially if you can set it up in such a way that it’s kind of something that’s a process that they go through one time. Like in the first session they might give their credit card information and then from then on you just kind of automatically charge them and they don’t have to worry about it, they don’t have to remember. So, I do feel like there’s a lot of value and convenience for the client as well as for the therapist. And yes, it does come at a cost. A certain percentage in credit card fees, and I think it really is a personal preference but also it depends on your business model if that’s a cost that you feel you can take on or if it’s worth the fees. I believe there are some other options that honestly I know little bit less about and there might be some HIPAA violations, but one is an app that I believe is made for therapists, and I don’t use it because I don’t know that much about it, but I think there are more and more apps out there like this that do cut back on the credit card fees and it is HIPAA compliant, so there are possibly some other ways to get paid that are convenient and use modern technology like apps that clients can use. I can throw out a name but I don’t know that much about it.

Ken: Yeah. Well, it’s interesting with credit cards you don’t have to worry about HIPAA as much. There’s an exception in HIPPA for financial transactions because otherwise essentially no bank would ever be able to run any healthcare related transaction.

Kari: Right. Yeah.

Ken: Because there’s always a name and a billing party.

Kari: Yeah.

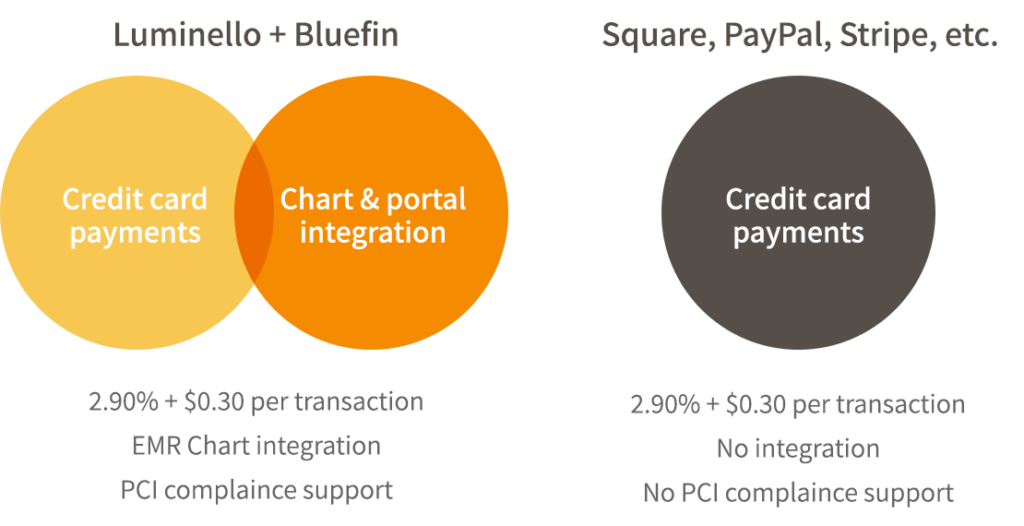

Ken: The system would fall apart. So, there is protection in HIPAA for it. On the flip side, with credit cards, you then have to think about PCI compliance, which is the credit card industry’s way of protecting credit card data. So it’s really important as a practice that you think about what your policies are going to be for who is going to enter that credit card number, whether it’s an app, or integrated within the EMR, or just run in a standalone kind of way, and I highly recommend that the patient or client enter the credit card and that the clinician as a practice policy never enters the credit card number. Because then the PCI standard is the burden on the clinician and on the practice is reduced by like 98% just by that one small detail. But it’s a really big detail for the credit card industry because they know that there isn’t somebody else getting in the way and having access to the credit card, and that’s what they’re really protecting, is that credit card number.

Kari: Yeah.

Ken: So, that is something to think about with setting up credit cards and ideally, whatever merchant or whatever system you’re using, you are going to have to attest yearly to being PCI compliant, and if you have a system that works well for you and that makes that process go really quickly, that’s great! Sometimes the first year takes a little time to go through the questionnaire because you’ve never done this before, but then in the following years it’s just, “Has anything changed?” No. Okay. Submit. So, it’s a minor point to think about.

Kari: Yeah.

Ken: Okay. So, the other thing to think about with the cost of credit cards that comes to mind is if you don’t take credit cards and you have a patient or client who ends up never paying their bill, how much does that cost you, and you have to crunch your own numbers and see. And that does happen. We can come back to that a little bit later. Okay, let’s talk a little bit about how do you actually bill your clientele? Let’s give a few different scenarios. One is standard weekly therapy client. One is someone you’re seeing for therapy, but just as needed or every other week or just anything non-weekly and then for MedChecks. I’ll speak to the MedChecks. Why don’t you start with your weekly clients, how often do you bill them?

Kari: Yeah. I require a payment at the time of a session. That’s my policy. I prefer, from my cash-flow perspective, on the business side but it also eliminates the need for me to come up with a system to remember to bill clients or send invoices. I like to just have everything done the day of. It used to be in-person right then and there we might do the fee exchange. Now it’s all done remotely and I have credit cards on file. So, I require weekly payments. Of course, there are always exceptions. If for whatever reason a credit card is expired or something like that, it’s okay from a clinical perspective for there to be exceptions. But I personally prefer a weekly cadence for that kind of stuff, less to remember for me for the therapist.

Ken: At the end of the day do you run all the transactions at once or is it while the client is in the office?

Kari: No. As a remote therapist, since I’m only working over video, it’s at the end of the day. It used to be in the session with the client they would actually hand me a credit card and I would swipe it. But now I have a whole different system, I don’t use the swiping machine, so now it’s just at the end of the day. But I do know of therapists who do accept payments monthly. Like, they send out an invoice and then they might run it through credit card or the client might send them a check. So, I would be curious to hear what you do or what your experience has been.

Ken: Sure. So, the way I do it is if it’s say, MedCheck or this is somebody I’m seeing for therapy but not on a particularly regular basis, not weekly. Typically run those soon after the session. Their credit card is already on file so I tend to batch them and just do them all in a bunch and just look at the accounts receivables. And I can run the credit card right from there. But there’s a feature that we use that’s called AutoPay. So, if you create an invoice and you set an AutoPay date, then the system actually is now running the credit cards automatically. So, that’s even nicer because I don’t need to do anything and it gets the job done, and I get notified if it has been successful or not on that day. So, that’s where my practice has gone lately. If it’s a weekly therapy patient, I tend to bill them once a month because it’s fine. Even with the AutoPay feature, each time you run a credit card there’s a small fee just for the act of running it. But it’s tiny. It’s just cents. That’s not the main reason. It’s more just simplification so that somebody gets used to just paying once a month or having it automatically charged once a month instead of weekly. But I can see either, and I would be curious in that community what percentage of therapists are billing monthly versus weekly. I would guess there’s a fair number of both camps and you can make an argument in either direction for that.

Kari: Yeah.

Ken: Even before being remote, I hardly ever met with anyone who wanted to pay by check.

Kari: Yeah.

Ken: First of all, it uses session time. People would like fiddle in their purse looking for the check book and write down, and I’m just sitting there and it’s like, tick, tick, tick, you know? I hate to use session time for that.

Kari: Right.

Ken: So, that hurts one component. And yeah, cash did not come up. So, it was mostly being able to have the ability to accept credit cards. At that time not a lot of people were doing it so I felt like it was a marketing advantage for my practice. But now, so many people do it. It’s just expected that you take credit cards. The other thing that’s nice about taking credit cards is that a fair number of my patients have HSAs or FSAs through their work and they get a debit or some sort of card to use with that. And so being able to accept that makes their administrative burden significantly less in terms of them not having to file for reimbursement. The same way as if they wrote me a check from that account or from their own personal account. Okay, so this makes sense, so somehow or another the money comes in, either you’re going to the bank or taking pictures of your checks and sending them in for your deposit, or you run the credit card, or the credit card is automatically run and in your business checking account the money appears. So, I guess we should go back a step and say you need to set up a business checking account. And I don’t think they’re that complicated. It’s just a checking account associated with your business tax ID. So, maybe we should go back a step and say you should set up a tax ID first. And that takes about one minute.

Kari: Yeah.

Ken: And so if anyone is wondering, you can just Google “IRS create my own tax ID for my business” and it will take you right to the IRS page and it is a few steps. And you should never be using your social security number to bill your patients or clients for obvious identity theft concerns. So, if you’re a solo practitioner, i.e. you’re not doing any special paperwork to incorporate or become an LLC, if your state allows it, get an EIN (employer identification number). It’s your business tax ID. And you take that, the IRS will auto generate a PDF for you in five seconds that has your new number. And then you go to your bank and you say, “I’d like to open up a business checking account, and here’s my EIN number” and the reason you should do this and not just have money come in to your personal checking account, it is a mess if it goes into your personal checking account because if you ever get audited or you just need to go to a bank to get a loan, or for your accountant for taxes at the end of the year, you really don’t want all that information being mixed. It will take you so much time to un-mix it. You might as well just do it right from the beginning. Okay, so, that’s your tax ID, you got your business checking account, and you set up your Merchant account to deposit into your business checking account. And I guess you should say you should set up a Merchant account if you want to accept credit cards. And you can do that through various third party apps through EMRs or a standalone solution. Okay. However you want to do it, you link it to your checking account and then the money comes in. However, that does not mean all that money then goes out. So, let’s talk about what comes first before being able to access that money. This partially depends if you’re a solo proprietorship or if you’re let’s say, a corporation or LLC. But first thing that comes to my mind is paying taxes. So, I’m curious, tell me how you pay your business taxes.

Kari: Well, my process is that I put aside a certain percentage of my income and save that. I should also say I have a business savings account as well as a business checking account.

Ken: Good one.

Kari: And I also have an accountant that helps me figure this out. And I think just depending on how complicated your taxes are, and how you file, it could be really useful to have an accountant. You can also figure this out in other ways or through other means. I have an accountant who tells me what percentage of my income I should be putting aside, and I do that. So, any time I’m getting ready to pay myself whatever is in there, in the checking account, I do the math and I put aside a certain percentage of that, put it in my savings, and that will later go towards paying quarterly taxes. That’s basically money that’s if it doesn’t belong to me. It belongs to the state and the federal government. So, that’s how I make sure I have funds for taxes. Does that align with you?

Ken: Yeah. And how do you actually pay your tax? How does it get out of your savings account and over to the government? I’m curious.

Kari: Well, this is where it’s helpful for me to have an accountant who sends me the information with what my estimated quarterly payments are, and along with that, links to pay. I’m in California, so to pay California taxes as well as federal taxes. And then I’m literally online. I do everything online. I click these links and I follow the tide. It’s really straightforward. And at the end of all that, I type in the account information, the savings account information, then the money is taken out of the savings account by either the IRS or California. And it’s all electronic and actually really quick and easy especially once you’ve done it once. And if you pay quarterly, you’ll do this four times a year so you get familiar with the process.

Ken: Yeah. So, the IRS runs a site called EFTPS I think that’s what you’re referring to and that’s how you can tell the IRS how much to extract from your checking or savings account. And you can set that up to be automatically done quarterly, or each quarter you can go in and put in a unique amount. And same in California, the state franchise tax board has a similar kind of thing, and most states I presume try to make it easy for them to get their money.

Kari: Yeah.

Ken: So, that is as a solo practitioner because you are at the end of the year filling out a schedule C under taxes. Hence, you need to report how much to pay your estimated taxes throughout the year. And if you didn’t pay your estimated taxes, two things happen: One, you have a big tax bill. And second, is that you get penalties and fines because the government is expecting that you will pay as the money comes in. And for solo practitioners, that’s quarterly. And with the one caveat in the second quarter, your estimated tax payment is due before the end of the quarter. And that’s purely so the government can have the money faster. So, that’s as a solo practitioner. My practice is structured as a corporation so it’s slightly different. In a corporation, I’m the employee of the corporation as well as the owner. And so I have to run payroll for myself, which is a weird concept. And so I use a payroll service, and I tell them how much to pay me and to pay my assistant based on the hours that we’ve worked that month. And then the payroll service automatically files all the tax forms that need to be done for corporation. And it is not cheap that service, but it is so worth it because I’ve less than no interest in filling out monthly tax forms for the state and the government. And they just do it with a few clicks. And in that sense, because I’m paying myself monthly, taxes are being automatically withheld monthly. And so a portion of the money comes out of the business checking account and goes straight to the government automatically and then a portion goes into personal checking account. And so that’s how the process works for corporation or that kind of structure. Okay, so you’ve paid your taxes, but before you do that you also have to think about your business expenses and how are you going to pay those. So, I’m curious, how do you pay your business expenses?

Kari: It has changed over time. So, earlier on I was probably more organized with it, and now a little bit less so. So, earlier on, and I think this is a good idea, especially getting started. I think it’s good to have it written down somewhere what your monthly expenses are, so that might include rent, internet, any subscriptions like Psychology Today, water sources, if you have that in your office, anything you can think of. Have that written out whatever that totals up to. Before I pay myself I would make sure to keep that amount in my checking account because a lot of times too with those monthly payments it sort of just gets taken. You set up automatic payment at some point and things get taken from your checking account so you always want to make sure that you have that money there. And so accounting for that, whatever is left after that I would pay myself. The other thing I wanted to say too, before I pay myself, I also put aside every time I go to pay myself I put aside extra money on top of what I’m putting aside for taxes on top of what I’m putting aside for monthly expenses, I also just put aside extra that will eventually go towards a retirement fund that I contribute to on April 15th at the end of tax season. And that’s something you do have to think about especially if you’re a sole proprietor starting to contribute to retirement. And so, I save extra money every month for that out of habit. If for some reason I really need cash for some business expense, maybe there was an extra training that I wanted to go to or something like that. It’s not urgent but I try to make it a habit to save for retirement. So, after I put aside money for all those things, then what’s left goes into my personal checking account, since my business and my personal account are all through the same thing, it’s just a simple transfer. For me, I do that once a month. I know some people who do that once a week. That is just too much math for me at too quick of a pace so I like to do that monthly. And that’s how eventually I end up seeing the cash in my personal checking.

Ken: Okay. That brought up a couple of thoughts. One is I think retirement is a good podcast for us to be thinking about and how to think that through.

Kari: Yeah.

Ken: But a little out of scope for today.

Kari: Yeah.

Ken: But it’s a great topic to think about. Second is a business credit card. I think it’s just worth mentioning that’s probably easiest to pay any recurring bills you have on the business credit card. Again, don’t put it on your personal credit card because it is a mess if you get audited. Your accountant needs to see your expenses at the end of the year. And if it’s your personal and your business expenses combined, it’s just asking for a lot of time to be wasted. So, set up a business credit card that is automatically paid from your business checking account and everything will be in a nice package. Of course, some things like rent is hard to pay through a credit card, so for those kinds of expenses most banks offer online bill pay and you do that from your business checking account again so you can keep everything in the same place. Okay, so, going back to my scenario, I went a little bit out of order. I don’t run payroll on myself until I’ve paid all my business expenses. Because I better make sure they’re paid then I run payroll. And a big chunk of that goes to the government first, and then I get the scraps that are left over. Going back to the budget that you are talking about, I think it’s worthwhile to have both a monthly and an annual budget. Because there are some annual expenses that are usually bigger than your standard monthly expenses. What comes to mind for me, as a corporation, the State of California has a minimum payment that’s owed regardless, just for the joy of running a corporation, so I have to set aside for that, your professional license renewal. For me, it’s every two years, and then I have to renew my DEA certification every three years, and then any professional organizations that you’re a part of, like the American Academy of Child and Adolescent Psychiatry or the American Psychiatric Association. I’m curious what kind of annual expenses do you have?

Kari: Yeah. I think it’s the Liability Insurance.

Ken: Yes. Okay.

Kari: And then I think every two years you have to renew your license, which is a big expense. And yeah, any memberships like American Psychological Association. Those are the top ones that come to mind.

Ken: Okay. Then there’s kind of the, not quite one offs, but like going to a conference for example, that could be very expensive. But even doing CME or CEUs online, they add up depending how many you need to do, so you should have a budget for that as well in addition to your monthly rent and things like that.

Kari: Yeah.

Ken: That way on a yearly basis, I mean, I guess some people would put aside one twelfth of those expenses every month into their savings, that’s one way to do it, or they just know that in some months of the year your pay is going to go down because you’ve got to pay those business expenses first.

Kari: Yeah, right.

Ken: Okay. So, I think we should talk a little bit about how do you keep track of all of this and what system do you use? One is, how do you know how well your business is doing, how do you generate those kinds of reports, at the end of the year when your accountant says, “Great, send me what you got.” What do you send? You know, it sounds good. Great, take it from here. But you have to send them something. So, I’m curious what your process is Kari. What do you send?

Kari: Yeah. I use QuickBooks. That’s another monthly expense I have to pay. And through QuickBooks is how I can track you know my business expenses and sort that for my accountant. I do have to confess that this is an area that I find confusing and stressful. I would choose to pay someone to help me here, and for me that’s actually more budget friendly than spending the time. So, I actually have a bookkeeper who helps reconcile my QuickBooks to make sure that everything looks the way that my accountant needs it to make sense of my books. As you can see, this is why I hire someone to help me. And at the end of all of that, at the end of every year, my accountant get’s a report called A Profit and Loss and that’s how she can figure out what was my gross income, what were the business expenses that were deductible and not deductible, what is my net income after all of that, what is my taxable income, so I keep track of all that though QuickBooks but I do have help and I recommend it for someone. It’s actually not a huge expense and it saves me a lot of time because to me, this kind of stuff when it comes down to all the things there are to possibly know, it’s like speaking a foreign language. So, I do the best that I can keeping track of things and sorting things in QuickBooks and then at the end of it all I have someone look it over for me. How do you keep track?

Ken: Well, the way I did it when I first started out was, I actually hired a QuickBooks expert to come train me. I realized after how many years of being in school, I had no clue how to do any of this. And it was the first time that I felt like I was back in middle school. They went through it like, ”Now Ken, pretend you’ve got this amount of money and this expense. Go into QuickBooks and enter it.” And I would be like, *toot, toot, toot* did I do it right? And they’d be like, “No.” [Laughs]

Kari: [Laughs]

Ken: But anyway, I learned through trial and error. So, that first year I was in practice. I did have the QuickBooks person look over what I was doing and tell me how I was screwing up. And then I faired it out from there. This was something for Luminello we’re looking to build long-term so that way all of the data is already within your practice and so we’ll do it for you. I’ll at least do as much of it as we can but that’s down the road. So, yeah, I use QuickBooks and I reconcile it with my checking account every few days so that way nothing gets out of line because when I started out I was like ah, reconciliation *boring* couldn’t care less. And I would go months and then it would be like totally not matching. And I would stare at the screen like a deer in headlights going, “I really should have not waited this long” and it would be a painful process to figure out what was entered twice or what wasn’t entered. And now I just do it every few days and my bank has a way to send that info directly into QuickBooks and so I can see it instantly.

Kari: Wow.

Ken: So, I spend like probably two minutes on this every three days as opposed to like a day and a half on it on a weekend monthly the way I was doing it before. Then at the end of the year, the accountant, since I run a corporation, I have to give them profit loss, a balance sheet, a general ledger, and the reconciliation to prove that I’ve done it. Because the accountant is going off the data you’re giving them. They’re not auditing you. And they want to know they’re working with data that is clean.

Kari: Exactly.

Ken: They don’t want to put themselves in a position where they’re going to get accused of saying well, you prepared a tax return and you didn’t pay the government enough. So it’s in their interest to make sure your data is clean as well as your own interest.

Kari: Exactly. Yeah.

Ken: I think we have taken this one as far as we’ve probably got. I’m sorry, earlier on I teased with dealing with patients and clients who don’t pay, but I think we should save that for another podcast. And we can also just talk about how do you get paid more while you’re at it?

Kari: Yeah.

Ken: And how to think that through by taking this as a good primer in the mechanics of billing. So, thank you very much. Always appreciate your time.

Kari: Thank you.

Ken: And look forward to talking again soon.

Kari: Me too. Take care.

Ken: Bye, Bye.

Kari: Bye.